The crypto wave is inescapable. Conversations on crypto are everywhere on the internet, from Twitter to Reddit to Instagram. Household superstars like Lebron James now star in advertisements for crypto companies. In the Middle East, Qatar is set to host the 2022 FIFA World Cup with popular crypto trading platform Crypto.com as the official sponsor.

It is nearly impossible to circumvent all the crypto talk, as its flourishing market surpasses USD 2 trillion in trade volume. So, what exactly is crypto and why has it become so big, and so controversial in countries like Egypt?

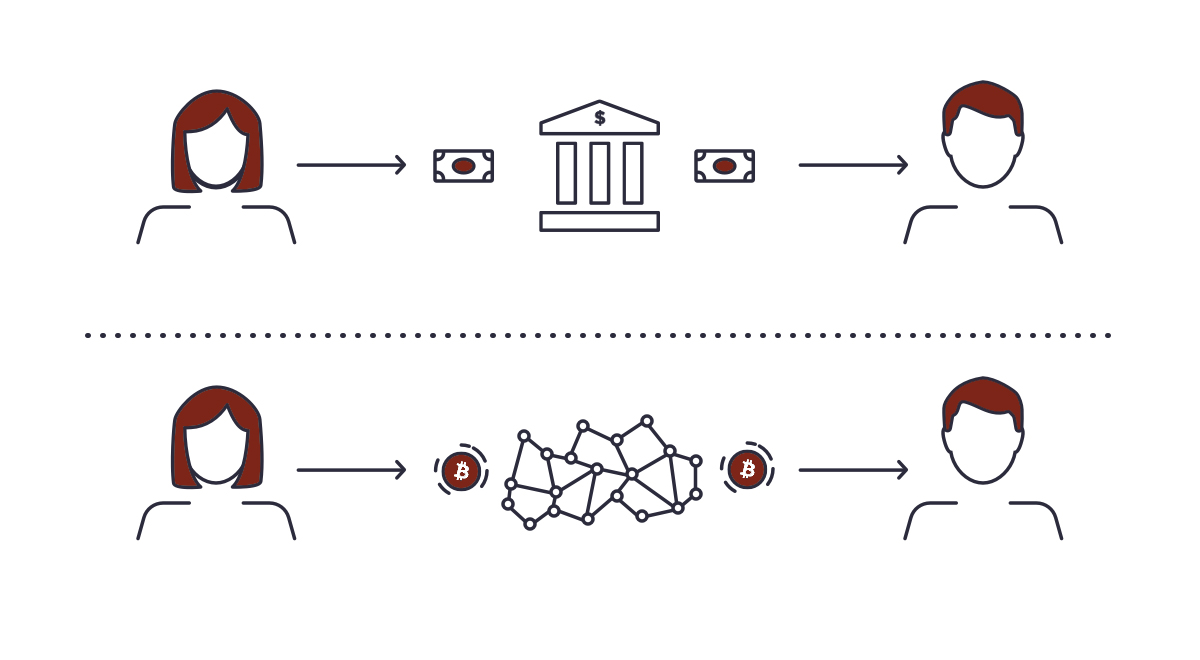

In short, crypto is an overarching term for blockchains and cryptocurrencies.

“Bitcoin, Ethereum, Dogecoin … these are all cryptocurrencies. And blockchain is the backbone of cryptocurrency. [Blockchain] is a decentralized ledger, which means no one owns it or decides what goes on it,” explains Cesare Fracassi, professor of finance at the University of Texas.

In a centralized economy, which all countries currently are, every transaction made is funneled and recorded through the ledger of a centralized authority – usually banks and the state. Blockchains and cryptocurrencies cut out such middlemen. For example, Bitcoin was minted as a digital currency in a way that transactions required no centralized authority.

From the perspective of Egypt’s government, which functions primarily in a centralized system, the crypto wave remains an obscure risk to its economy and security.

THE CRYPTO-CRIME CONUNDRUM

Despite being criminalized, crypto trading continues to exist in Egypt. A study conducted in 2021 by Triple A, a crypto consultancy firm, estimated that 1.7 million Egyptians own some form of cryptocurrency.

While a minuscule number within the overall Egyptian population, the statistic indicates an increasing trend in demand for digital currencies.

“The idea of a decentralized currency and investing in it is a bit like investing in the future,” says Ahmed Mostafa, a computer science graduate from the American University in Cairo.

Since cryptocurrencies are banned in Egypt, Ahmed uses a shared offshore account with a trusted friend, to invest in cryptocurrencies abroad.

“I know that stocks are a bit more stable and there are also tons of ways to invest money in general. But for me, someone who doesn’t have that much to invest, the best way was to invest in something that has had huge growth over the last couple of years, enough to make a decent amount of money back from a smaller amount of money invested than I would have in other forms,” Ahmed tells Egyptian Streets.

Ahmed notes that those who do not have the opportunity for an offshore account often use person-to-person (P2P) transfers.

“P2P is also a good substitute for those living local looking to invest, but they can’t really profit from it here as long as they’re in Egypt,” explains Ahmed.

In other words, there is no way for cryptocurrency holders in Egypt to monetize their investment without an offshore account. It is, then, idle in his cryptowallet until a solution occurs.

Nonetheless, Egypt could come to learn from the global crypto-mania and seize the opportunity for a digital era in their economy.

CASHLESS BUT NOT CRYPTO?

Egypt has clearly expressed its stance against cryptocurrencies. In a warning statement, The Central Bank of Egypt (CBE) highlighted that Egypt does not deal with cryptocurrencies due to their volatile nature and anonymity. From a security perspective, the Ministry of Foreign Affairs cites virtual and encrypted currencies as a security threat to Egypt.

There are also traces of truth to these statements. The global growth of crypto, which remains in its budding stage, has fueled crimes, from fraud to terrorist funding to money laundering.

Globally speaking, the process of creating cryptocurrencies like Bitcoin is severely detrimental to the environment. In Bitcoin’s case, the cryptocurrency requires a transaction confirmation known as ‘proof of work’. In other words, computers must solve compounding complex math problems – often requiring several computers to crack the code at the same time.

This proof of work mechanism is drastically drains energy far more than anticipated. A study conducted by BBC determined that in 2021, Bitcoin consumed the same amount of energy as the Netherlands.

In comparison, traditional transaction methods, such as Visa rely on far less energy. Visa is capable of 1,700 transactions per second compared with Bitcoin’s four.

Yet, Egypt’s restrictions can only quell the crypto wave to a limited extent. As the country’s fiat currency faces devaluation, the number of Egyptian crypto users is expected to continue to rise, as investors search for higher-profit currencies.

So, is it a matter if you can’t beat them, join them? Not exactly.

In 2018, CBE announced it was studying the potential of minting a state-controlled digital currency. A digital Egyptian Pound would offer both the government’s centralized control while providing the market with a cashless.

The introduction of a digital fiat will not necessarily quench the current thirst for crypto, as the incentive in crypto is its high value. However, it could potentially render the digital advantages of crypto obsolete. Furthermore, an Egyptian digital currency would resolve the country’s concerns with anonymous criminal trading and economic volatility.

And perhaps the CBE was correct in its warning of volatility. On 9 May, the global cryptocurrency market experienced a severe crash that it is yet to recover from – initiated from the crash of Terra and Luna coins, two popular forms of cryptocurrencies. The ripple effect of that crash has led to the loss of billions and large-scale concerns over a potential bubble burst – once more raising questions on formally regulating cryptocurrency.

As it stands, cryptocurrencies at their current stage are not a viable alternative to fiat currency, physical or digital. As an unregulated and decentralized form of payment, Egypt will find it difficult to trust its value. The cryptocurrency era is a remarkable technical achievement that will most definitely reshape the global digital economy, but to become a widely accepted form of payment in Egypt, it will need to address the security concerns it faces, not just in Egypt, but globally.

Names have been changed for safety reasons.

Comment (1)

[…] كيف تواجه مصر موجة التشفير العالمية؟ […]